This can help you move from vague estimates to a clearer view of your actual options before you make a decision.

Explore non-recourse financing to make exercising affordable

Even if you’ve figured out the best course of action, paying for exercising out of your own pocket can be very expensive.

That’s especially true with NSOs because exercising can trigger ordinary income taxes before you have any cash from selling your shares. If your company’s 409A valuation has already increased, the combined cost of your strike price and taxes may be more than you want, or are able, to pay out of pocket.

If you qualify, Secfi’s non-recourse financing may help cover the cost to exercise your stock options, including taxes. You don’t make monthly payments, and repayment is tied to a future liquidity event, such as an IPO or acquisition.

Because the financing is non-recourse, your personal assets aren’t on the line if your company doesn’t exit or the shares become worthless. So you may be able to exercise earlier and start the clock toward long-term capital gains treatment without taking on the risks of a traditional loan.

Learn more about Secfi’s non-recourse financing to see how it works.

Get support from equity strategists who work with startup executives and employees every day

NSO tax planning can get complicated quickly, especially if you’re weighing exercise timing, 409A changes, tax rates, financing, and your personal financial goals at the same time.

Secfi’s team works with startup employees on these decisions daily. We’ve supported people from startups to make decisions that can improve their equity outcomes.

Whether you’re trying to understand your exercise cost, compare timing scenarios, or decide whether financing could make sense, our team can help you look at the decision with more context before you act. Our wealth team can also support your broader financial planning goals.

How Secfi helped a startup employee figure out what to do with her NSOs and exercise her stock options

Amanda didn’t know much about equity when she joined a software startup. But a few years later, her company gave employees the option to convert their ISOs into NSOs.

At first, the conversion seemed sensible. NSOs can give employees more flexibility if they leave the company. But Amanda quickly realized there was a trade-off: NSOs are generally taxed less favorably than ISOs, which meant the decision could affect how much she kept after taxes.

She started researching NSO taxes and capital gains, but still found it difficult to know what decision made sense for her situation. Amanda wanted to own her equity, but she didn’t want to take out a bank loan, put her savings at risk, or affect her debt-to-income ratio when she was thinking about buying a house.

After a coworker recommended Secfi, Amanda finally felt like she understood her options.

“Secfi was one of the only websites I could find that could give me accurate calculations,” she said. And she appreciated the friendly team and fair offer to finance the cost of exercising.

Using Secfi’s non-recourse financing made her feel more comfortable exercising, knowing it kept her personal finances safer than a traditional loan.

For the full case study: Why a startup employee used Secfi to buy her stock options.

Testimonials are specific to an individual Client’s experience and may not be representative of all Clients. Unless otherwise indicated, Clients offering a Testimonial do not receive compensation and their statement does not present a conflict of interest.

Make a plan to maximize favorable NSO stock options tax treatment

This guide helped you understand and see real examples of how you can handle NSO stock options tax treatment. While there are many options available to you, trying to make the best choice for your situation alone can be intimidating.

That’s why it’s worth modeling your options before you exercise with our free AI equity assistant Mave, or reaching out to our team if you want hands-on support.

FAQs

Are NSOs taxed twice?

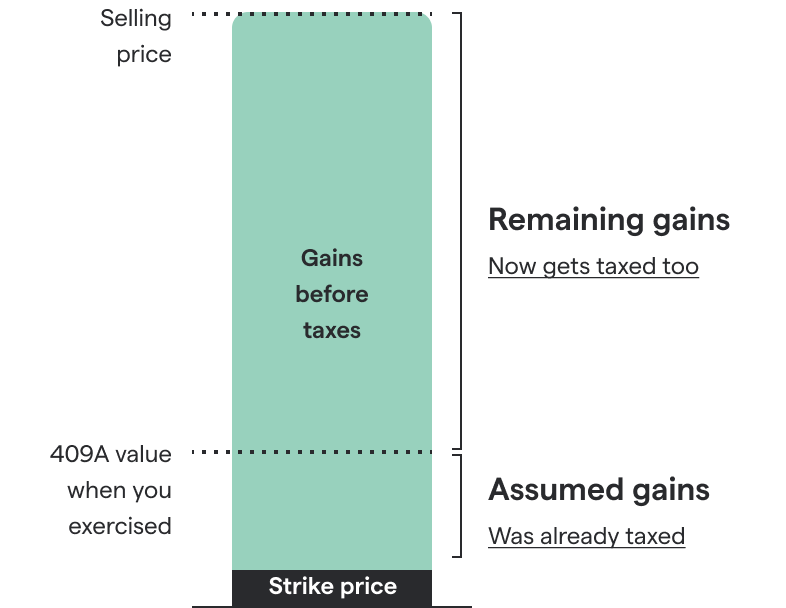

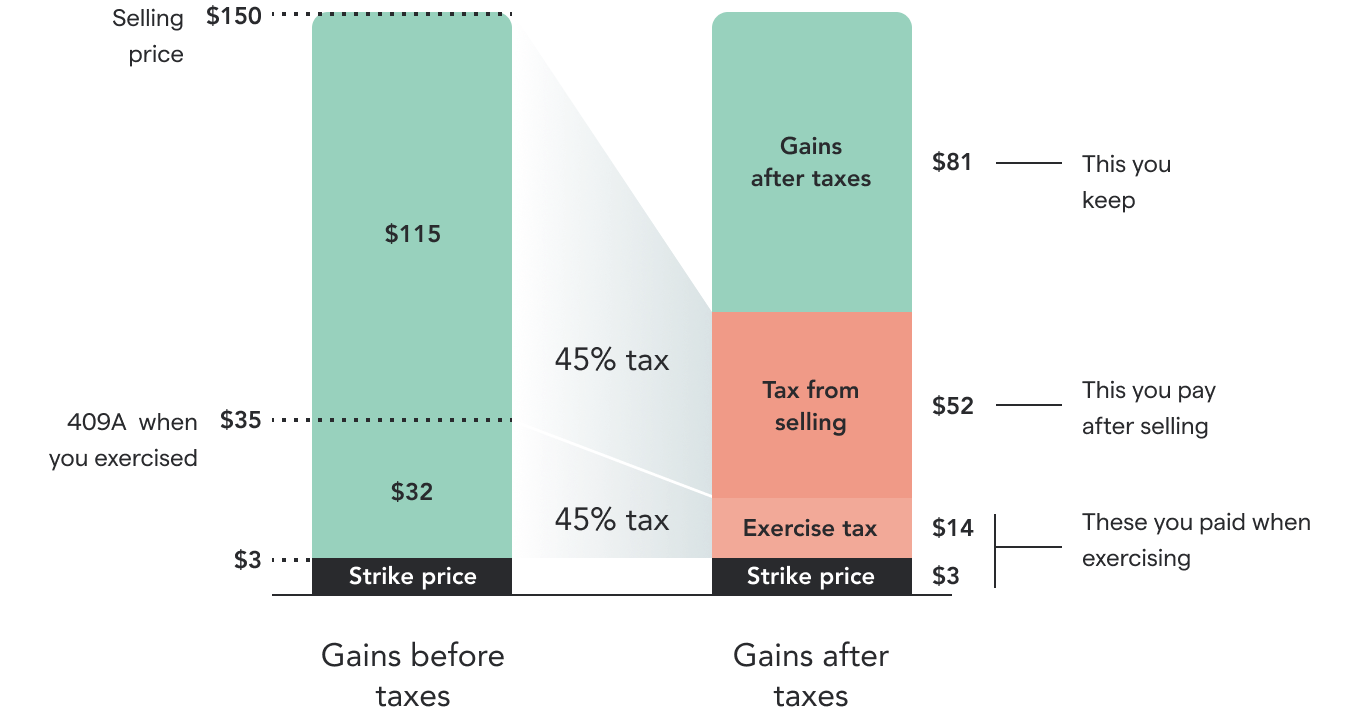

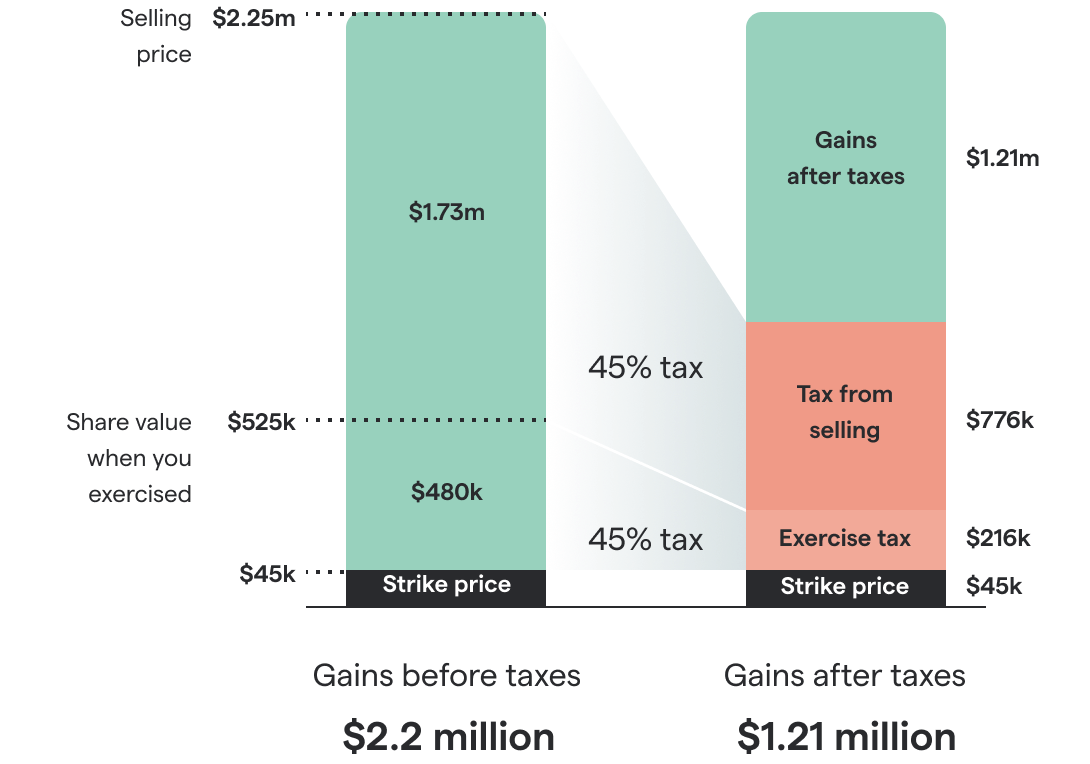

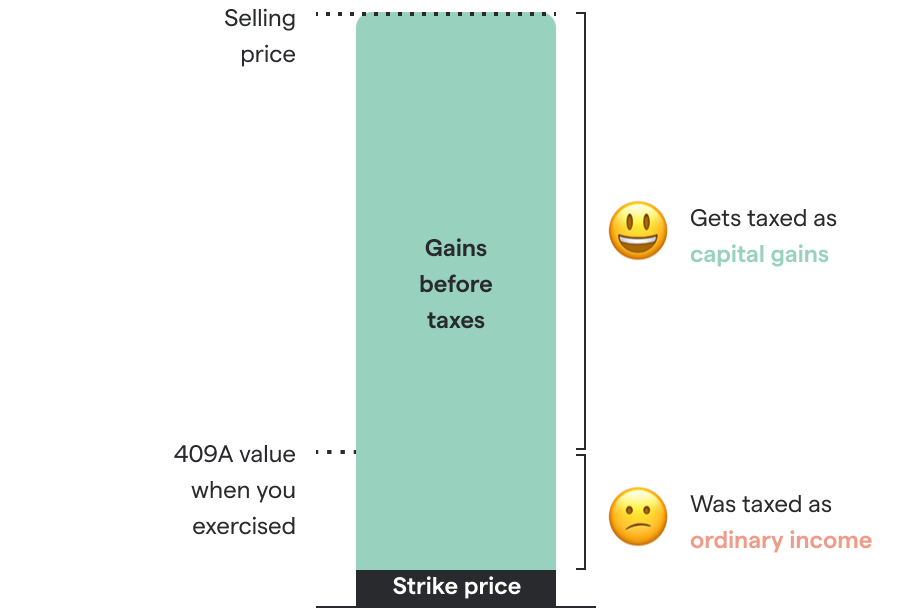

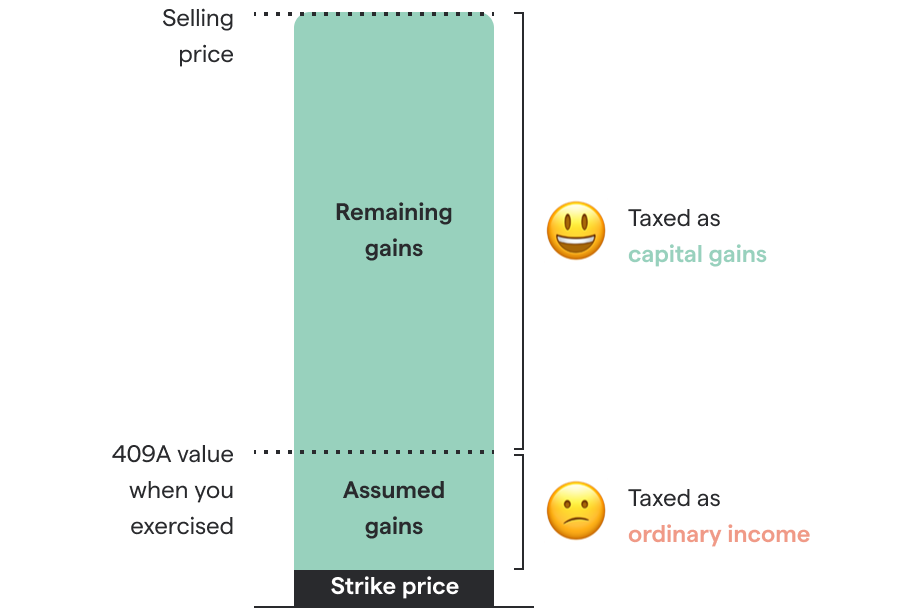

NSOs can create two taxable moments. First, when you exercise your NSOs, the difference between your strike price and the fair market value is generally taxed as ordinary income. Later, if you sell the shares for more than their value at exercise, you may owe taxes on that additional gain.

This doesn’t usually mean the exact same gain is taxed twice. It means different parts of your gain may be taxed at different points. Maeve, Secfi’s AI equity planning assistant, can help you model how those taxes may apply to your specific grant.

Does NSO have taxes?

Yes. NSOs can trigger taxes when you exercise and when you sell. At exercise, the spread between your strike price and your company’s fair market value is generally taxed as ordinary income. At sale, any additional gain may be taxed as capital gains or ordinary income, depending on how long you held the shares.

Because the tax bill can be significant, it’s worth modeling your NSO exercise costs with an AI equity planning tool like Secfi’s Maeve before making a decision.

How are stock options treated for tax purposes?

Stock options are usually taxed based on the type of option, when you exercise, and when you sell the shares. NSOs are generally taxed at exercise if there is a spread between the strike price and fair market value. ISOs may qualify for more favorable tax treatment, but they can also trigger alternative minimum tax, or AMT.

If you’re not sure how your options may be treated, Secfi can help you model different exercise and sale scenarios with our free AI equity assistant Maeve.

Do you have to pay taxes when you buy stock options?

If you’re granted stock options, you usually don’t pay taxes when you receive them. With NSOs, taxes usually come into play when you exercise, which is when you buy the shares. If the fair market value is higher than your strike price, the difference is generally taxed as ordinary income.

You may also owe taxes later if you sell the shares for a gain. It’s worth modeling different scenarios with a tool like Secfi’s free equity assistant Maeve, or speaking with equity and tax specialists before making any major decisions.

What’s the ISO vs NSO tax difference?

The main difference is that ISOs may qualify for more favorable tax treatment if you meet certain holding requirements. NSOs generally don’t qualify for those same tax benefits, so they are usually taxed as ordinary income when you exercise if there is a spread.

That said, ISOs can be more complicated because they may trigger AMT. NSOs are often more straightforward, but they can still create a large tax bill. Secfi’s AI equity assistant Maeve can help you compare different option exercise scenarios so you’re not relying on rough guesses.

How can I help reduce taxes on NSO stock options?

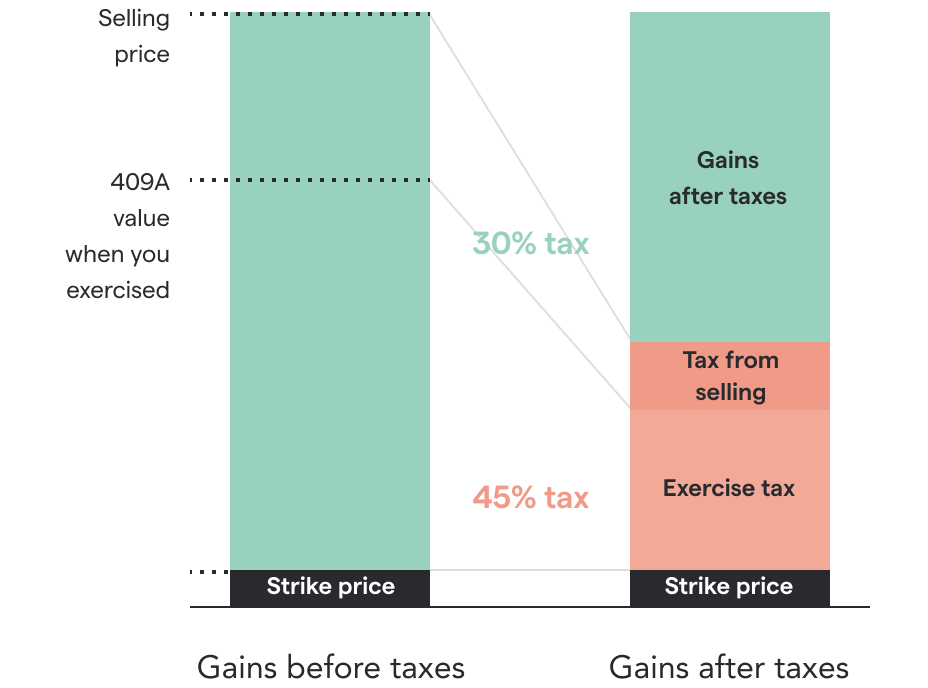

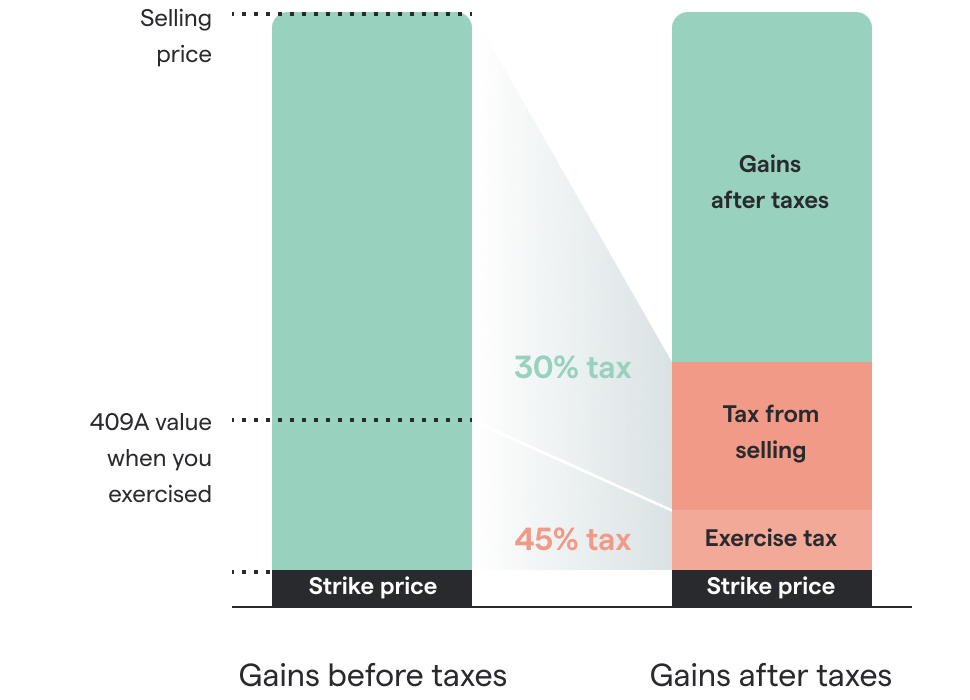

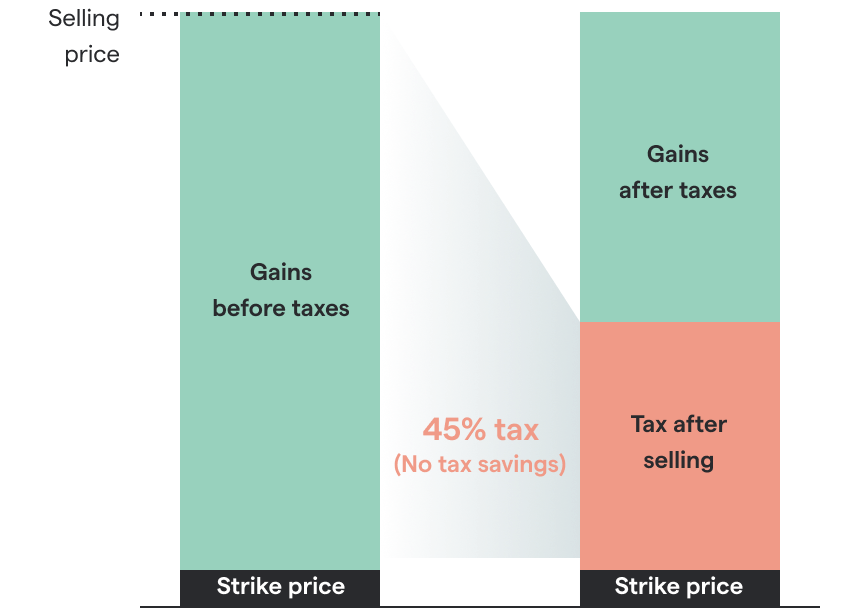

One way to potentially reduce NSO taxes is to exercise earlier, when the spread between your strike price and your company’s fair market value may be lower. If you hold the shares for more than one year after exercising, any additional gain after exercise may qualify for long-term capital gains treatment.

But exercising early can be risky and expensive, especially if your company never exits or the tax bill is high. Secfi can help you model the trade-offs with our AI equity assistant Maeve, and explore whether non-recourse financing may be available to help cover exercise costs and taxes.

The tool shown here uses artificial intelligence and is for illustrative purposes only and not necessarily indicative of future results and there is no guarantee that similar results can be achieved. The information provided by the tool is not professional advice and is not intended by Secfi, Inc., its affiliates, and Secfi representatives, to be deemed as investment, legal, tax or other professional advice or recommendations of any kind, or to form the basis of any decision to do or to refrain from doing anything. Secfi does not review the accuracy or completeness of the information provided to us within the tool.