How to help avoid AMT when exercising options

10 min

0 result

San Francisco native (yes, really). @uw and Lowell High alum. I like to nerd out on fintech, stock options and taxes.

If you work at a pre-IPO company that’s taken off and your incentive stock options (ISOs) have appreciated significantly, you’re probably going to get a substantial tax bill once you exercise.

That tax burden — known as the alternative minimum tax (AMT) — could cost you a lot more than your exercise price. It might be even more than that. In principle, there’s no limit.

Because this often comes as a shock, a lot of our clients ask: how can I help avoid AMT when exercising my stock options?

It’s a fair question, especially if you just found out that exercising your options initially priced at, say, $15,000 leads to a tax bill of $100,000.

In this article, we’ll cover:

Note: Secfi provides equity planning guidance, tools and financing so startup employees can own their stock options with confidence. If you’re looking to better understand what you can do with your equity, sign up to our free platform here: Get Started. As always, please consult a tax professional regarding your particular circumstance.

The alternative minimum tax (AMT) is a tax you may owe when exercising your incentive stock options (ISOs). It runs as a parallel tax system the IRS uses to make sure high-income earners pay a minimum amount of tax each year, regardless of how many deductions or credits they claim.

For startup employees and executives with ISOs, AMT is most commonly triggered when they exercise their ISOs and hold the shares instead of selling them in the same calendar year.

That's because the "phantom gain" from exercising ISOs can count toward your alternative minimum taxable income (AMTI). This phantom gain — sometimes called a preference item or an AMT adjustment — is the difference between your strike price and the company's fair market value (FMV) when you exercise.

So if your strike price is $1 and your company's fair market value (FMV) is $10, the $9 spread per share may be counted for AMT purposes, even if you haven't sold your shares or received any cash. (Note this is just an example, check with a tax expert to see what applies to your situation).

Your AMT builds up in parallel to your regular tax liability. Your regular bill is based on your regular taxable income, while your AMT bill is based on your AMTI. After all your taxable income and deductions are taken into account, you pay either your regular tax bill or your AMT bill, whichever is higher.

Usually, your accountant, CPA or tax software runs your regular income tax calculation next to your AMT calculation. Most years, your regular tax is higher than your AMT, so you don’t need to pay AMT and may not even know it exists.

For example, say your regular tax bill is $50,000, but exercising your ISOs pushes your AMT calculation to $70,000. In that case, you’d pay the higher amount: $70,000.

The extra $20,000 you paid because of AMT may become AMT credit. You may be able to use that credit in future tax years when your regular tax bill is higher than your AMT bill.

The diagram and example provided are for illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

But exercising ISOs can tip the balance. The larger the difference between your strike price and the company’s fair market value, the more likely you may be to trigger AMT. Other factors, such as your income, filing status, state taxes, and deductions, can also affect whether you owe AMT.

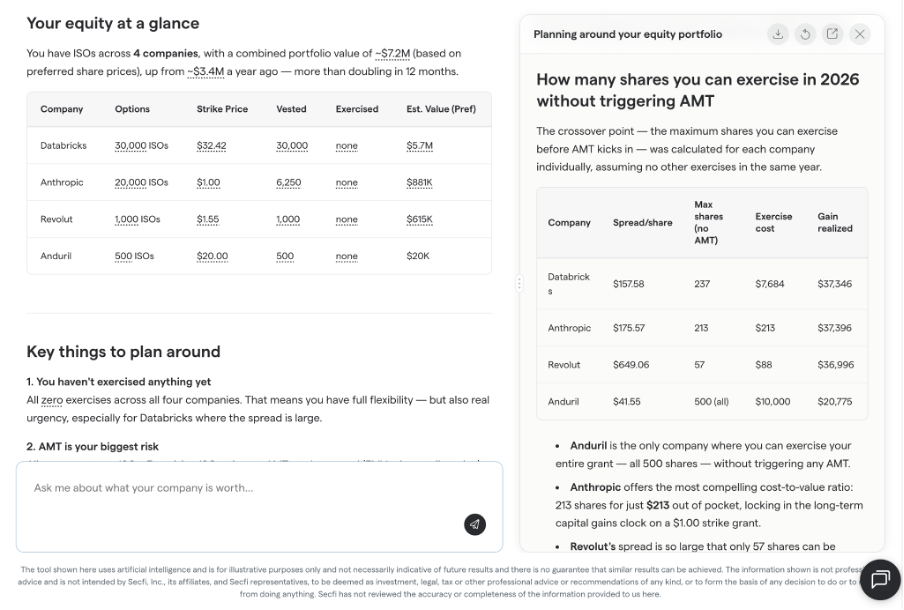

If you’re curious about whether exercising your options could trigger AMT, or how much your AMT bill could be, use Secfi’s free AI equity assistant Maeve. Enter your details and get a breakdown of your total exercise costs, including state and federal AMT.

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

We feel the way to avoid triggering AMT is by finding your AMT crossover point. That's the gap left between your current income and the amount that would trigger AMT.

Using your strike price and the current 409A valuation (also known as fair market value), you can calculate how many options you can still exercise this tax year right before you hit the crossover point and have to pay AMT.

It's a difficult calculation to do manually, so we built Maeve to help you figure how many shares you can exercise before hitting the threshold.

Exercising only the number of ISOs that keep you below your AMT crossover point can help you avoid paying AMT. And if you're optimistic about your company, it may be worth considering each year. But this approach has its limitations.

Using the AMT crossover point strategy, you can exercise a portion of your ISOs tax-free each year. But whenever the fair market value of your ISOs goes up, exercising each share counts more toward triggering the AMT.

Say that this year, you exercise 10% of your options to avoid AMT, but next year the 409A valuation of your company has gone up. Now the “phantom gains” of the remaining 90% of your ISOs is higher, and you reach the AMT crossover point sooner.

Because of that, instead of 10%, this year you may only be able to exercise 5% to 7% of your remaining options to avoid triggering AMT.

If your company continues to grow, every year you’ll be able to exercise fewer and fewer options without paying AMT.

So with this strategy, it can be difficult to ever get all of your options exercised.

(Note: This is just an example, it’s important that you speak to a tax professional regarding your particular circumstance.)

Say, theoretically, your company’s 409A valuation remains the same for the next 10 years and you can exercise 10% of your options each year without hitting AMT.

To pull this off, you’d have to stay at your company for 10 years to make it work assuming the 409A stays the same, which is unlikely if your company is growing.

Plus, the moment you leave your company, you may have just 90 days to exercise before you lose all your remaining ISOs. This is often referred to as the "golden handcuffs" problem that employees with a lot of stock options can run into.

You could exercise a small percentage of your options without hitting AMT for a while. But if your goal is to maximize the potential value of your ISOs in the event of a successful IPO, you need to exercise them at least a year before you sell them.

That could qualify you for long-term capital gains tax rates, which are lower than ordinary income rates.

Another option is to wait to exercise until the IPO and do what’s called a cashless exercise. Essentially, you can sell your shares on the same day that you exercise them and cover the cost of exercising (including the AMT you trigger) by selling a portion of your shares.

But in this case, you end up paying the highest tax rate possible on the portion you sell (i.e. you don't get that tax discount), so it’s also not ideal.

Finally, after your company has gone public, you could still exercise your options a bit at a time to avoid AMT. But again, you’d have to stay at your company the entire time it would take to do this for all of your shares and the more your company grows, the harder this becomes.

Next to that, once the company has gone public and your equity is sellable, it's risky to keep all of that wealth locked up in a single stock. Because even though your company has done very well, you never know when circumstances change.

Even with careful planning, you may not be able to avoid AMT entirely.

The frustrating thing about AMT is that you can owe taxes on gains that only exist on paper. Exercising your options doesn’t put cash in your bank account. But if your ISOs have increased in value, the difference between your strike price and the company’s fair market value may still count toward your AMT calculation.

The silver lining is that if you pay AMT, you may be able to recover some of that amount later through the AMT credit.

In general, if you pay more under the AMT system than you would under the regular tax system, the difference can become AMT credit. In future tax years where your regular tax is higher than your AMT, you may be able to use that credit to reduce your tax bill.

You’ll need to keep track of your AMT credit each year, usually with help from your tax professional or equity strategist from Secfi. There may also be limits on how much credit you can use in a single year, so it can take time to recover a large AMT payment.

For example, say your regular tax bill in a future year is $50,000, and you have $10,000 of AMT credit available from a prior year. In that case, you may be able to use that credit to reduce the amount you owe.

Example and diagram for illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

The main thing to know: paying AMT doesn’t always mean that money is gone forever. But it does mean you need to plan carefully, track your credit, and understand how long it may take to use it.

There are two other strategies which may be possible, but it depends on your specific situation.

Note: if your company has grown a lot since the time you were granted your ISOs, the 409A valuation has probably already increased and this isn't an option for you.

If you believe in the long-term viability of the company, and you think there's going to be a successful exit (i.e., an IPO or acquisition) where you can sell your shares at a gain, you can choose to exercise as early as possible, to minimize taxes and to start the 12-month clock on long-term capital gains.

Assuming your company is growing, the earlier you do it, the lower the 409A valuation (aka fair market valuation) will be. And that's the number determining your tax liability on exercise.

If your strike price is $1 per share and the fair market value is $1.05 per share, then you’ll very likely pay minimal taxes. In fact, if your company allows early exercising and you exercise your ISOs right after you get them, their strike price will be equal to the 409A valuation and you might not owe taxes on those ISOs at all.

The other option is to partner with a company that finances the cost of exercising (including any tax burden).

This is what we do at Secfi. Our financing is non-recourse, which means none of your personal assets or credit are on the line (like with a private loan). Instead, it’s backed by the shares you’re exercising.

You get to keep ownership of your shares and you’ll be able to exercise before your AMT burden continues to rise.

After the exit and when you've sold your shares you'll pay some of the gains you make back to us in the form of a fee. But in many cases — due to the tax savings you unlock — you're potentially better off than if you waited until the IPO and performed a cashless exercise.

Another benefit of financing is that once you own the stock, you don't have to wait around until an IPO if you don't want to. If you want to walk away from the company before the IPO, you can, while keeping your equity. You essentially get rid of your golden handcuffs.

Another possible way to cover the cost of exercising is to sell some of your private company shares through a secondary market, then use the proceeds to exercise the rest.

This won’t be available to everyone. Your company may restrict private share sales, require approval, or limit when employees can sell. Even if you can sell, there are tradeoffs.

The biggest one is that you give up future upside on the shares you sell. If your company’s value continues to rise and eventually exits successfully, you won’t participate in the gains on that portion of your equity.

So secondary markets can be helpful if you need liquidity, but they’re not a direct way to avoid AMT. They’re one possible way to fund an exercise decision, and whether they make sense depends on your company’s rules, your financial needs, and how much future upside you’re comfortable giving up.

Avoiding AMT entirely isn’t always possible. But with the right planning, you may be able to reduce your AMT, understand what it will cost to exercise, and decide whether exercising earlier makes sense for your situation.

Secfi helps startup employees model different exercise scenarios, understand the tax impact, and explore financing options if the cost of exercising is too high to pay out of pocket.

Here’s why employees from companies including Databricks, Canva, and Klaviyo choose Secfi.

The first step is understanding whether exercising your incentive stock options will trigger AMT, and if so, how much you may owe.

Maeve, Secfi’s AI equity planning assistant, helps you model different exercise scenarios based on your stock option details, income, company valuation, and timing. You can use it to ask questions like:

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

Maeve is powered with Secfi’s equity calculators, so you can check any assumptions you want to confirm. Getting set up with Maeve is easy. You can manually enter your information or connect with your Carta account.

For many startup employees, the issue isn’t whether exercising could be valuable. It’s whether you can afford the exercise cost plus the potential AMT bill. That’s where non-recourse financing may make sense.

Secfi’s non-recourse financing can help cover the cost of exercising your stock options, including the AMT taxes you may owe when you exercise. Unlike a traditional loan, your personal assets aren’t at risk. The financing is backed by your shares, and repayment is tied to a future liquidity event, such as an IPO or acquisition.

If your company has a successful exit, such as an IPO, acquisition, or other eligible liquidity event, you repay the amount Secfi financed plus a fee from the proceeds of your shares.

If your company doesn’t exit, or your shares don’t end up being worth enough to repay the financing, you don’t have to repay Secfi. Secfi takes on that downside risk. That’s the difference between non-recourse financing and a traditional loan: your repayment obligation is tied to the shares, not your house, savings, salary, or other personal assets.

Basically, we share in the potential upside if your company succeeds, but also take on the risk that there may not be enough value to repay the financing. That’s why non-recourse financing providers like Secfi are selective about the companies and equity we can finance. If your company does not exit, there could be additional tax consequences.

Non-recourse financing can be especially helpful if exercising now could reduce your future tax exposure, but paying the exercise cost and AMT out of pocket would create too much personal financial risk.

Even with calculators and AI modeling, exercising stock options is rarely a simple yes-or-no decision.

Your potential best move depends on income, your company’s 409A valuation, how many options you have, whether you plan to leave your company, your risk tolerance, and your timeline for a potential IPO or acquisition.

Secfi gives you access to equity strategists who work with startup equity every day. We can help you understand your exercise options, evaluate whether financing makes sense, and think through how AMT fits into your wider financial plan.

That combination matters because the right answer usually isn’t “avoid AMT at all costs.” In some cases, paying AMT now may be part of a strategy that helps you reduce taxes later, start the clock toward long-term capital gains treatment, or avoid a more expensive exercise decision in the future.

Amanda didn’t know much about equity when she joined a fast-growing software company. But when her company gave employees a choice to convert ISOs into NSOs, she started researching her options and quickly ran into AMT.

Everyone kept telling her “AMT is this mystical thing, you might have to pay it if you meet these things, but you probably don’t.”

But as someone who prefers making decisions with full information, that didn’t sit right.

“Secfi was one of the only websites I could find that could give me accurate calculations of AMT,” she said. Using our tools, Amanda got the information she needed. She started to understand the tax implications of exercising, including paying less AMT for ISOs by exercising early.

Amanda decided to exercise her options for the AMT benefit, but she didn’t want to use a bank loan to do it. With Secfi’s non-recourse financing, she covered the cost without affecting her debt-to-income ratio or putting her personal assets on the line.

Read Amanda’s full story to see how she made the call: Why a startup employee used Secfi to buy her stock options.

Testimonials are specific to an individual Client’s experience and may not be representative of all Clients. Unless otherwise indicated, Clients offering a Testimonial do not receive compensation and their statement does not present a conflict of interest.

AMT is complicated, but the worst-case scenario is usually not knowing it applies until after you’ve already exercised.

Before you exercise your incentive stock options, it’s worth modeling your potential AMT bill, comparing different exercise timelines, and understanding whether exercising earlier, exercising fewer shares, or using financing could make sense for your situation.

Secfi can help you see what exercising may cost, how AMT could affect your tax bill, and what options you have if the total cost is too high to pay out of pocket.

Start by creating a free Secfi account and adding your equity details to the platform. Maeve, Secfi’s AI equity planning assistant, can then use that information to model different exercise scenarios and estimate your potential AMT exposure. If you'd like additional guidance, you can also speak with Secfi’s licensed equity strategists about your next steps.

If you want to get a clearer picture of your AMT situation, you can start by using Secfi’s AI calculator Maeve and signing up to the platform to get an estimate of what you would owe: Get started.

The tool shown here uses artificial intelligence and is for illustrative purposes only and not necessarily indicative of future results and there is no guarantee that similar results can be achieved. The information provided by the tool is not professional advice and is not intended by Secfi, Inc., its affiliates, and Secfi representatives, to be deemed as investment, legal, tax or other professional advice or recommendations of any kind, or to form the basis of any decision to do or to refrain from doing anything. Secfi does not review the accuracy or completeness of the information provided to us within the tool.

You may be able to avoid AMT by exercising only the number of incentive stock options that keep you below your AMT crossover point. Your AMT crossover point is the point where your AMT calculation becomes higher than your regular tax calculation.

To find it, you need to look at your income, filing status, state taxes, deductions, strike price, and your company’s current 409A valuation. From there, you can estimate how many ISOs you can exercise before triggering AMT.

This can be hard to calculate manually, so Secfi’s AI equity planning assistant, Maeve, can help you model different exercise scenarios and estimate how many options you may be able to exercise before hitting the AMT threshold.

You can’t always avoid taxes when exercising stock options, but you may be able to reduce or delay them with careful planning. The right strategy depends on whether you have ISOs, NSOs, or RSUs, your company’s current fair market value, your strike price, your income, and when you plan to sell.

For ISOs, exercising earlier may reduce the difference between your strike price and the fair market value, which can lower the amount that counts toward AMT. Exercising before your company’s valuation rises may also help you start the holding period for long-term capital gains tax treatment.

Secfi can help you compare different exercise timelines, estimate your potential tax bill, and understand whether exercising earlier, exercising fewer shares, or using financing may make sense for your situation.

AMT is commonly triggered when you exercise incentive stock options and hold the shares instead of selling them in the same calendar year. The difference between your strike price and the company’s fair market value, sometimes called the bargain element or phantom gain, may count toward your AMT income.

For example, if your strike price is $1 and the fair market value is $10, the $9 difference per share may be included in your AMT calculation, even though you haven’t sold your shares or received any cash.

Whether you actually owe AMT depends on your full tax situation, including income, deductions, filing status, state taxes, and how many ISOs you exercise. You can use Secfi’s free AI equity planning assistant, Maeve, for a personalized estimate based on your situation.

Yes, exercising stock options early may reduce AMT if your company’s fair market value is still close to your strike price. That’s because AMT is driven in part by the difference between your strike price and the fair market value at the time you exercise.

If that difference is small, less value may count toward your AMT income. If your company grows and the 409A valuation increases, the difference between your strike price and fair market value may get larger, which can make exercising more expensive from a tax perspective.

Early exercise is not risk-free, though. You’re paying to buy shares in a private company, and there’s no guarantee those shares will become liquid or increase in value. That’s why it’s worth modeling the potential tax savings alongside the investment risk before you exercise. Try Secfi’s free AI Equity assistant Maeve to model your specific situation.

Yes, non-recourse financing may help cover AMT if you want to exercise your stock options but can’t afford the exercise cost plus the potential tax bill out of pocket.

With Secfi’s non-recourse financing, the financing can help cover the cost of exercising your options, including the AMT taxes you may owe. Unlike a traditional loan, your personal assets aren’t at risk. Repayment is tied to a future liquidity event, such as an IPO, acquisition, or other eligible liquidity event.

If your company has a successful exit, Secfi is repaid from the proceeds of your shares, including the amount financed plus a fee. If your company doesn’t exit, or your shares don’t end up being worth enough to repay the financing, you don’t have to repay Secfi from your personal savings.

To calculate AMT before exercising stock options, you need to estimate your AMT income and compare your AMT tax calculation to your regular tax calculation. The key input for ISOs is the bargain element, which is the difference between your strike price and the fair market value multiplied by the number of shares you exercise.

A simplified formula is:

Bargain element = (fair market value - strike price) × number of shares exercised

That amount may be added to your AMT income. From there, you apply AMT rules, exemptions, and tax rates, then compare the result to your regular tax bill. If your AMT bill is higher, you may owe the difference.

Because this calculation depends on your wider tax situation, it’s best to work with a purpose-built equity planning tool. Secfi’s AI equity planning assistant Maeve can help you estimate your AMT before exercising and compare different exercise scenarios before you make a decision.