How do you exercise stock options? Everything you need to know

15 min

0 result

Your startup equity could be worth a life-changing amount of money – but knowing when and how to exercise your stock options can have a huge impact on what you ultimately keep.

What are some reasons you may be interested in exercising options now?

No matter why you want to exercise your stock options, we’ve built this guide to help. We’ll cover:

Our goal is to help you make an informed decision about how, when, and if it makes sense to exercise your stock options. This guide is for informational purposes only and isn't a substitute for personalized tax or investment advice.

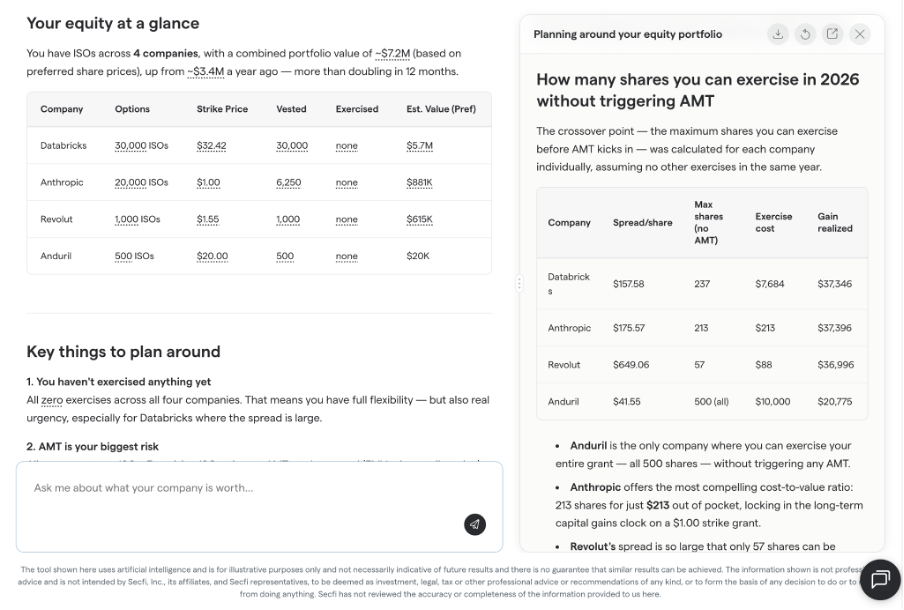

Do you want tailored information about your equity, your options, or the best way to maximize your wealth? Try our AI equity assistant Maeve for personalized equity and liquidity planning.

When you started working at your startup, you were given a stock option grant — a core part of your equity compensation — that detailed the type of stock options you would earn, as well as your vesting schedule, your strike price, and your grant date.

It may have been a long time since you looked at this documentation in detail, particularly if you’ve been in the role for a long time. But if you’re looking to exercise your options – or you just want to get a clear idea of your financial situation – you’ll need to revisit these grants.

Typically, there are three details that you should be clear on before you exercise.

One of the most important things you need to know is the type of stock option you have. This will impact how you’re taxed when you exercise (and if you later sell your options).

There are three major types of stock options:

At some startups, it's common to earn multiple types of stock options at once, particularly if the startup expects to go public in the near future. Each type comes with different tax implications, so it's worth knowing exactly what you hold before you do anything else.

Most options you receive will come with conditions that are outlined in your option grant. These will typically determine when and how you can exercise them, as well as how much it’ll cost you to do so.

It’s worth noting that you may have received refresher grants – i.e. additional options or RSUs – after your initial hiring package. These may differ from your original grant, so you’ll need to check both.

Some key information to look for include:

Your grant documentation will again be your source of truth here. While most options conform to similar conditions, to know anything for sure you’ll need to check your original grant. If you’re using a platform such as Carta, Shareworks, or Pulley, you’ll likely find the details there too.

Stock options are taxed when you exercise them, and taxed again when you sell them.

As a general rule, if your startup is growing, your tax bill is growing, too. So, if you’re confident your startup will successfully exit, it’s typically more affordable to exercise your stock options now, rather than waiting.

But precisely how much you owe will depend on the type of options you have, how much your company is growing, and what state you live in. So, your tax bill is highly personal and can be quite complex to work out by yourself.

Rather than trying to work it out by yourself, it helps to have a tool walk you through it. Our secure AI equity assistant, Maeve, can give you the tailored information you need. Try it here.

Once you have all the necessary information at hand, here are the 5 key steps to exercise:

It can be useful to talk to an equity advisor to help you make a decision about your options. Or you can use Secfi’s AI equity assistant, Maeve, to easily model different scenarios and related costs.

There are three main types of stock options (ISOs, NSOs, and RSUs), and they’re taxed differently at exercise.

RSUs are the simplest, so let’s start there. RSUs are earned (rather than purchased), and are treated like a cash bonus with tax authorities.

For example, you might be granted 1,000 RSUs that vest over four years, with a one-year cliff. On your one-year work anniversary, 25% of the grant (250 RSUs) vests. The remaining RSUs then vest on a regular schedule, such as monthly or quarterly, over the next three years.

At many private companies, RSUs are subject to a double-trigger vesting structure. The first trigger is your time-based vesting schedule. The second trigger is a liquidity event, such as an IPO or acquisition. This means that even after your RSUs have vested, you may not actually receive the shares until the second trigger occurs.

Once both triggers have been satisfied, the vested RSUs are converted into company shares and delivered to you. At that point, the value of those shares will depend on the company's share price.

Tax authorities treat RSUs like a cash bonus because they assume the company’s shares have value on the day you get them. So, in this example, tax authorities would view the $25,000 of shares you receive in the same way as if your company had given you a $25,000 cash bonus.

Companies that issue RSUs typically calculate taxes on your behalf, and automatically withhold them from your paycheck, similar to a cash bonus. At publicly traded companies, the company typically sells a portion of your shares to cover your tax liability.

So, in the example above, your company might sell 100 shares to cover your tax liability, and give you the remaining 150 shares as common stock – the standard type of ownership share typically held by employees and founders.

Late-stage, pre-IPO startups occasionally issue RSUs, and will tell you how much you owe in taxes as they vest.

ISOs and NSOs are similar, because you have to buy them before you own them. If you’re working at a high-growth startup, your cost to exercise ISOs and NSOs will likely rise every year, due to taxes.

For example, let’s say you’re issued a stock option grant for 100,000 shares of either ISOs or NSOs, at a strike price of $1 per share.

Four years later, you’ve completed a standard four-year vesting schedule, and you’re eligible to buy all 100,000 shares. At that point, the startup’s fair market value (also known as a 409A valuation) has gone up – from $1 per share when you started at the company, to $10 per share:

Here, ISOs and NSOs start to work a little differently. With ISOs, you may owe taxes under the alternative minimum tax (AMT) system. With NSOs, you’ll owe taxes under the income tax system.

All things being equal, ISOs are typically preferable to NSOs, due to AMT treatment. This can allow employees to defer a portion of their tax liability and potentially benefit from lower long-term capital gains tax rates if the shares are held long enough.

How much you’ll owe will depend on how many shares you exercise, where you live and any state taxes you might owe, and the assumed gain between how much you paid, and how much they’re worth – at least on paper.

Like any investment, stock options carry risk. There’s risk in abandoning them, there’s risk in exercising them, and there’s risk in selling them.

As a startup employee, you’ll need to assess those risks, and decide whether you want to invest in your company.

On the other hand, many startups fail. When a startup fails, founders typically liquidate the company’s assets, and use those assets to pay back company debt, and in some cases, pay back their investors.

For people who exercise stock options, the major risk is that the company they’ve bought shares of fails, and they lose their investment.

There’s also a related risk: that you exercise your stock options and incur a stock option-related tax bill that you can’t afford.

This happened during the dot-com bust to tech workers like Jeffrey Chou. He was a Cisco engineer who exercised his stock options but saw the value of the company’s shares plummet on the public market shortly afterward. By the time tax season came around, he faced a $2.5 million tax bill, and no way to pay it.

In Chou’s case, he would have likely experienced a better outcome by performing a cashless exercise, which is where you exercise your stock options and immediately sell some or all of them on the open market, in what’s effectively treated like a single transaction by tax authorities. (Note: Performing a cashless exercise also means you’ll pay the highest possible tax rate on the transaction.)

The risk of finding yourself underwater on AMT taxes is particularly high if you’ve joined a later-stage company that’s preparing to exit, and your strike price is relatively high. AMT tax liability is calculated on the day that you exercise, which is a risk if the underlying value of the shares decline during the exit.

Note: Make sure you estimate your AMT liability before you exercise, and that you can afford your AMT bill. Occasionally, people exercise their stock options and hope that their shares will rise in value, so they can sell them later and cover their AMT. The major risk is that share value will instead fall, and you face an AMT bill you have no way of paying.

Every year, startup employees abandon billions of dollars worth of vested employee stock options, by failing to exercise their options after leaving their jobs.

For example, consider Tesla. In 2008, less than two years before the company would go public, employees forfeited 2.8 million shares of company stock, which they could have exercised at an average price of 73 cents per share.

Today, those shares are worth an estimated $14 billion, following the company’s 5-1 stock split in 2020.

There are a number of reasons why employees abandon their stock options:

The major risk to abandoning some or all of your stock options is that the company experiences a successful exit, and you lose out on the upside of your stock options.

Investors are familiar with the risk when selling shares – namely, that the investment will continue to grow in value, and the investor will miss out on upside.

On a smaller scale, that’s true for startup employees holding pre-IPO stock options, and pre-IPO shares. Every year, startup employees sell billions of dollars worth of pre-IPO shares to accredited investors through company-organized tender offers and on secondary marketplaces.

Sometimes, employees turn to secondary markets and stock buybacks as a way to raise enough money to purchase the rest of their stock options. In doing so, they’re losing out on potential upside that they could experience during an eventual exit.

Similarly, employees might also lose out on upside if they refuse to sell post-IPO. That’s why it makes sense to work with a financial professional to build a plan for how and when you want to sell your equity.

By now, you’ll have a good idea of how to exercise your stock options, how to estimate your total cost to exercise, and how to weigh your own unique risks and potential rewards.

So, finally, how do you pay for stock options?

Here are the four most common ways that people pay to exercise their stock options, with related risks:

1. Cash. The simplest way to exercise stock options is with cash out of pocket. If you can afford it, it can make sense.

Risk: If the company fails, you could lose your entire investment. You risk tying up money in an illiquid investment, and losing out on potential upside from a more balanced portfolio of investments.

2. Traditional loans. With a loan, you won’t have to risk your own money to exercise your stock options. Depending on who you loan money from, you may need to immediately begin paying interest on the loan.

Risk: If the company fails, gets acquired at a deep discount, or experiences a disappointing IPO, you will still need to repay the loan – with the interest on top.

3. Secondary markets. Some people use secondary markets to sell a portion of their stock options, so they can raise enough money to exercise their remaining stock options and pay related taxes.

Risk: It could take a long time to find a buyer on a secondary market, and buyers may drive a hard bargain. You may end up giving up more stock options than you’d like, sacrificing potential future upside.

4. Non-recourse financing. There are two major benefits to using non-recourse financing in a way that Secfi offers. Firstly, the company gives you the money necessary to exercise your options and to pay any related taxes. Secondly, the company also assumes most of the downside risk in the transaction, so if the startup fails and the startup’s stock options are deemed worthless, you don’t have to pay back the loan.

Risk: You’ll pay fees to the non-recourse financing company, meaning you’ll lose some of your potential upside upon exit. There may be some additional tax consequences depending on your tax situation.

There’s no right answer when it comes to paying for your options. Each choice comes with its advantages and risks.

That’s why it’s useful to discuss your situation with a specialist equity advisor who can help you make the right decision for you.

As you’ve seen, exercising your stock options is not a straightforward decision. It typically requires a lot of cash up front – and you’ll likely have a large tax bill to pay too.

Exercising comes with significant costs, often to the tune of tens of thousands of dollars. As such, it’s not a question of cost alone, but of risk too. There’s no guarantee that the startup will exit. And if you’re paying out of pocket to exercise, you may not get that money back.

At Secfi, our founders experienced the challenges of exercising first-hand. They were working in a startup, but they didn’t have the cash they needed to exercise. That’s why they started Secfi, to help other people in similar situations.

Now, we help startup employees and executives navigate the complexity of their stock options, thanks to our combination of planning tools and expert guidance.

We also provide financing solutions to support you to exercise your options without a significant financial burden up front.

Here’s how we can help:

Most people only start thinking about their stock options when there's a deadline looming, for example, after leaving a company and discovering they have just 90 days to exercise.

The challenge is that generic online advice can't tell you what exercising will actually cost. Your tax bill depends on factors such as your option type, income, state of residence, and company valuation.

If you need personalized guidance, Secfi's equity strategists can help you evaluate the costs, tax implications, and risks of exercising, and whether it makes sense in the first place.

Or, if you'd like to explore different scenarios yourself, try Maeve, our AI equity assistant. Maeve uses your actual equity data and live market signals to provide personalized tax estimates and model potential outcomes.

Try Maeve now and instantly get the details you need to act on your options with confidence.

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

If you decide to exercise your options, Secfi offers non-recourse financing designed specifically for pre-IPO equity. This way, you can exercise without having to cover the costs out of pocket.

Employees looking to exercise typically need to cover:

Most employees have significant paper wealth but not the cash to cover it.

That’s why it can make sense to work with Secfi, to help cover the cost of exercising and the associated taxes. As the financing is non-recourse, you won’t need to pay it back out of pocket. In fact, you won’t need to pay it back at all if the company does not have a successful exit or its valuation decreases.

Instead, repayment comes from the proceeds of any successful exit. Your assets aren’t at risk at all, which makes it a much less risky choice than traditional loans. There may be some additional tax consequences if your company fails to exit.

Plus, at Secfi, we can also help you sell your shares on the secondary market. We’ll help you understand whether you’re eligible, and then we can act as a broker to connect you with buyers.

Alongside non-recourse financing and equity strategy, we also offer specialist wealth advice designed specifically for tech employees.

If you work at a startup or tech company, your options will likely only be one part of your total wealth. If you’re looking to maximize your wealth, there may be other strategies available to you beyond your equity decisions.

At Secfi, our specialist financial advisors can help you create a financial plan with a personalized roadmap to grow your wealth. You’ll get a dedicated advisor who can help you build a tailored financial strategy that includes your company stock – so you can be sure you’re doing everything you can to increase your wealth.

Get in touch with our financial advisors to find out more.

Victor, a senior engineering leader at a fast-growing startup, wanted to exercise his stock options. But the upfront cost – including a significant AMT bill – made the decision financially daunting.

Although he believed in the company’s long-term potential, he didn’t want to tie up his savings or take on personal financial risk through a traditional loan.

Instead of footing the bill himself, Victor chose Secfi’s non-recourse financing solution, which covered both the exercise cost and associated taxes without requiring personal collateral or monthly repayments.

Beyond the funding itself, he valued Secfi’s educational support and guidance through the complex equity and tax process. Not only did it help him protect his personal finances, it gave him greater confidence in managing his startup equity and long-term wealth-building strategy.

Read more: Why this engineering leader chose Secfi to finance his stock options

Testimonials are specific to an individual Client’s experience and may not be representative of all Clients. Unless otherwise indicated, Clients offering a Testimonial do not receive compensation and their statement does not present a conflict of interest.

Exercising stock options is very similar to purchasing shares in any other company. You now own stock in the startup, and get to decide when it’s time to sell the shares.

Of course, you may need to wait until there’s a buyer for your shares. This could be in the form of a tender offer, stock buyback, a secondary marketplace, an acquisition, or when your startup goes public.

If you hold your shares for at least one year after exercising them, you'll generally qualify for the long-term capital gains tax rate when you eventually sell them, which is typically lower than ordinary income tax and short-term capital gains tax rates.

Note: If you exercise ISOs, you’ll need to additionally hold onto your shares for at least 2 years after they were originally granted to qualify for long-term capital gains.

Once you’ve exercised your stock options, it’s worth periodically checking to see the company’s current fair market value in your stock options benefits administration platform – such as Carta or Shareworks — to see the company’s current fair market value (also known as a 409A valuation).

Of course, deciding if and when to sell your shares is a highly personal decision. Consult with your CPA or licensed financial professional for personalized advice.

Want to get personalized advice on your equity and wealth? Talk to an equity strategist today.

The tool shown here uses artificial intelligence and is for illustrative purposes only and not necessarily indicative of future results and there is no guarantee that similar results can be achieved. The information provided by the tool is not professional advice and is not intended by Secfi, Inc., its affiliates, and Secfi representatives, to be deemed as investment, legal, tax or other professional advice or recommendations of any kind, or to form the basis of any decision to do or to refrain from doing anything. Secfi does not review the accuracy or completeness of the information provided to us within the tool.

If you’re planning to leave your company, it’s important to understand your post-termination exercise window — many startups only give employees 90 days to exercise vested stock options before they expire. Exercising earlier may also reduce your tax burden and start the clock for long-term capital gains treatment.

You still have options. Employees commonly use savings, traditional loans, secondary market sales, cashless exercises during an exit event, or specialized stock option financing to cover exercise costs and taxes. The right strategy depends on your company’s stage, your risk tolerance, and your liquidity needs.

ISOs, NSOs, and RSUs each have unique tax treatment. ISOs may qualify for favorable long-term capital gains treatment but can trigger AMT, while NSOs are typically taxed as ordinary income upon exercise. RSUs are taxed when shares vest because employees receive them automatically rather than purchasing them. Understanding these differences can help you avoid unexpected tax bills.